Introduction

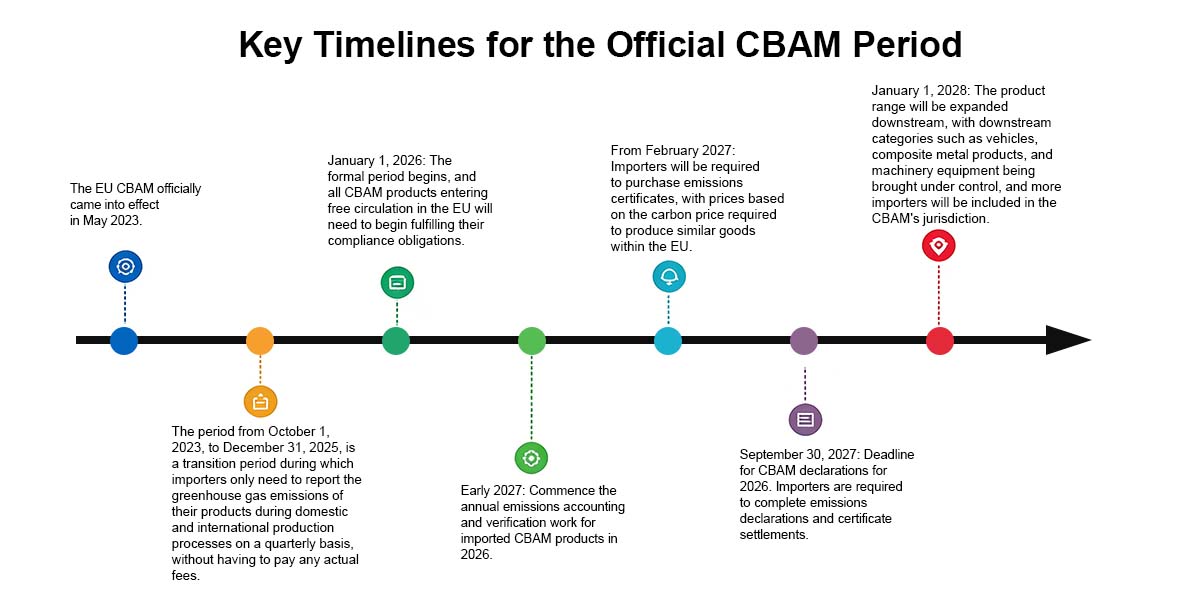

Effective January 1, 2026, the EU Carbon Border Adjustment Mechanism (CBAM) will officially conclude its transition period and enter the substantive levy phase. This means that the EU will formally impose carbon tariffs on the carbon emissions associated with imported products such as steel, aluminum, and cement.

As one of the first six sectors covered by the Carbon Border Adjustment Mechanism (CBAM) and a core product of China’s exports to Europe, the steel industry is facing a “green reshuffle” in global trade. Meanwhile, according to data from the International Energy Agency (IEA), carbon emissions from the global steel industry account for 7% to 9% of total emissions from the energy system. Undoubtedly, the steel industry remains a carbon-intensive sector, and the global low-carbon transition in this sector is accelerating. Technologies such as hydrogen shaft furnaces and Electric Arc Furnace (EAF) Short Process have moved from the conceptual stage to large-scale implementation, with a number of leading steel companies successively bringing their low-carbon production lines online. Concepts such as “low-carbon steel” and “near-zero-emission steel” are becoming increasingly clear, and Environmental Product Declarations (EPDs) are emerging as the “green passport” for international trade.

Therefore, in future international trade, buyers and sellers must not only focus on steel grades and prices, but also pay close attention to the underlying “carbon content”—which will determine the compliance and hidden costs of future supply chains.

In this article, CSMC will break down the key changes in the 2026 CBAM regulations, the logic behind carbon cost calculations, and how to see through various “green labels,” helping readers make truly informed procurement decisions amid the uncertainty.

1. Core Framework of the CBAM Policy

The EU Carbon Border Adjustment Mechanism (hereinafter referred to as “CBAM”) is a key institution under the EU's “Fit for 55” climate policy framework. Its core objective is to eliminate the cost disparity between the EU’s strict carbon constraints and relatively lenient carbon policies outside the EU by imposing a levy on specific imported products commensurate with their embedded carbon emissions. This ensures that imported goods bear carbon costs equivalent to those of EU domestic producers, thereby mitigating the risks of industrial relocation and carbon emissions shifting (i.e., “carbon leakage”) caused by carbon price asymmetry. At the same time, the introduction of CBAM can also have a potentially positive impact on international emission reduction efforts outside the EU. To avoid paying CBAM fees, countries exporting products to the EU can establish their own carbon pricing systems (with prices aligned with those of the EU Emissions Trading System (EU ETS)) or achieve this goal through decarbonized production.

To refine the CBAM system, the European Commission published a package of amending proposals on December 17, 2025. The proposals include a series of detailed adjustments regarding carbon accounting, free allowances, and the pricing of CBAM certificates, aimed at addressing carbon leakage loopholes exposed during the transition period and enhancing the system’s enforceability and regulatory rigor. The package also includes a draft proposal to expand the list of covered goods to include steel- and aluminum-intensive downstream products as of January 1, 2028, potentially adding more than 180 product types. While these amendments do not alter the fundamental framework or core logic of the CBAM, the detailed adjustments—such as changes to carbon accounting default values and free allowance benchmarks—will still have a significant impact on Chinese companies operating abroad.

The EU Carbon Border Adjustment Mechanism (CBAM) officially entered into force in May 2023. A transition period runs from October 1, 2023, to December 31, 2025. During this period, importers are only required to report, on a quarterly basis, the greenhouse gas emissions associated with the production of relevant products both domestically and abroad; they are not required to actually pay any fees. Pursuant to Regulation (EU) 2023/956 of the European Parliament and of the Council of May 10, 2023, establishing a Carbon Border Adjustment Mechanism (CBAM), this regulation sets forth the reporting obligations under the Carbon Border Adjustment Mechanism during the transition period from October 1, 2023, to December 31, 2025.

Effective January 1, 2026, the mechanism will enter its full implementation phase. EU importers must begin purchasing the corresponding number of emission certificate based on their annually reported emissions, with prices determined according to the carbon cost incurred for producing similar goods within the EU. Additionally, the European Commission announced that it will publish the first quarterly reference price for Carbon Border Adjustment Mechanism (CBAM) allowances on April 7, 2026, and is currently developing a unified CBAM allowance trading platform. The initial price will be calculated based on carbon market data from the first quarter of 2026 and will be made public through the EU CBAM registration system.

Starting in 2028: The CBAM is expected to be expanded to cover more downstream products (such as automotive parts, machinery, and home appliances), further broadening its scope. As free carbon allowances are gradually phased out, the enforcement of the CBAM will become more stringent.

2. CBAM Cost Calculation Mechanism

For exporters, the focus has shifted from “whether to prepare for CBAM” to “how exactly CBAM is calculated, how the resulting data affects corporate costs, and the extent of that impact.” The most immediate impact of CBAM is an increase in import costs. CBAM is rapidly evolving from a “policy concept” into a “real cost” for businesses; essentially, it transforms the external costs of carbon emissions into quantifiable financial costs.

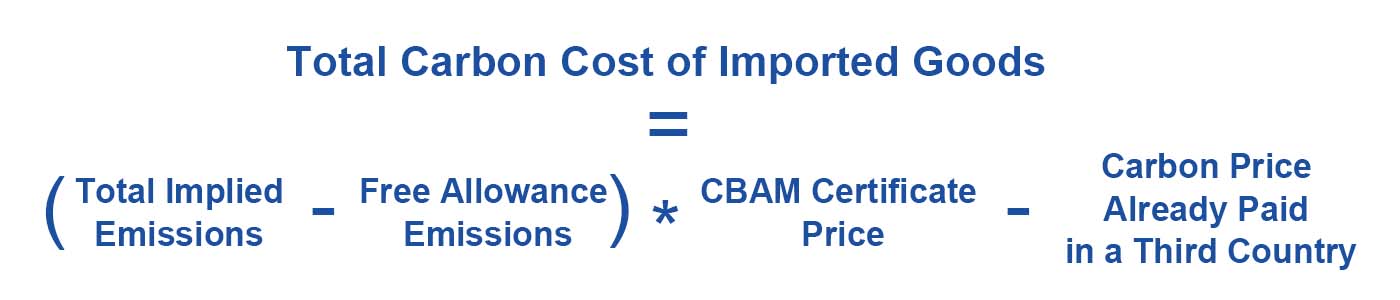

The core formula for CBAM is:

Total carbon cost of imported goods (CBAM levy) = (Total implied emissions of the product – Free Allocation Allowance (FAA) for comparable EU products) × CBAM certificate price – Carbon price already paid in a third country

Product-implied emissions refer to the carbon dioxide equivalent generated per ton of steel during the production process. There are two methods for determining these values: if an exporting company can provide actual emissions data verified by a third-party organization recognized by the EU, it may use the “actual value”; if such data cannot be provided, the “default value” set by the EU must be used. According to the detailed rules issued in December 2025, the default values for steel products in 2026 will be 10% higher than the country-specific average, 20% higher in 2027, and 30% higher in 2028. This means that for steel products for which carbon data has not been prepared in advance and for which an Environmental Product Declaration (EPD) has not been obtained, the implied emissions will be significantly overestimated. For long-process steel exported from China, emissions calculated using default values may be 20% to 50% higher than actual values, directly leading to a multi-fold increase in carbon tax costs.

Duty-free quota (FAA) = Total mass of imported goods × Specific Implied Duty-Free Allowance (SEFA) per ton

The free allowance is calculated using the CBAM factor, the cross-sectoral adjustment factor, and the CBAM reference value for the product.

For the free allowance, if an importer uses the supplier’s actual data to calculate carbon emissions, the free allowance (SEFA) = the product-specific implied free allowance from the production process + the implied free allowance for relevant precursor materials. If the official CBAM default values are used for calculation, SEFA = CBAM factor × cross-sectoral adjustment factor × the CBAM reference value for the product.

CBAM certificate prices are adjusted based on the price of EU carbon market allowances

Carbon costs already paid in a third country: If the exporting country has imposed a carbon tax on steel production or implemented a carbon trading mechanism, companies may apply for a tax credit by providing valid documentation. However, it should be noted that China’s national carbon market has not yet included the steel industry, which means that for steel exported from China to the EU, the carbon costs paid in the country of origin are essentially zero.

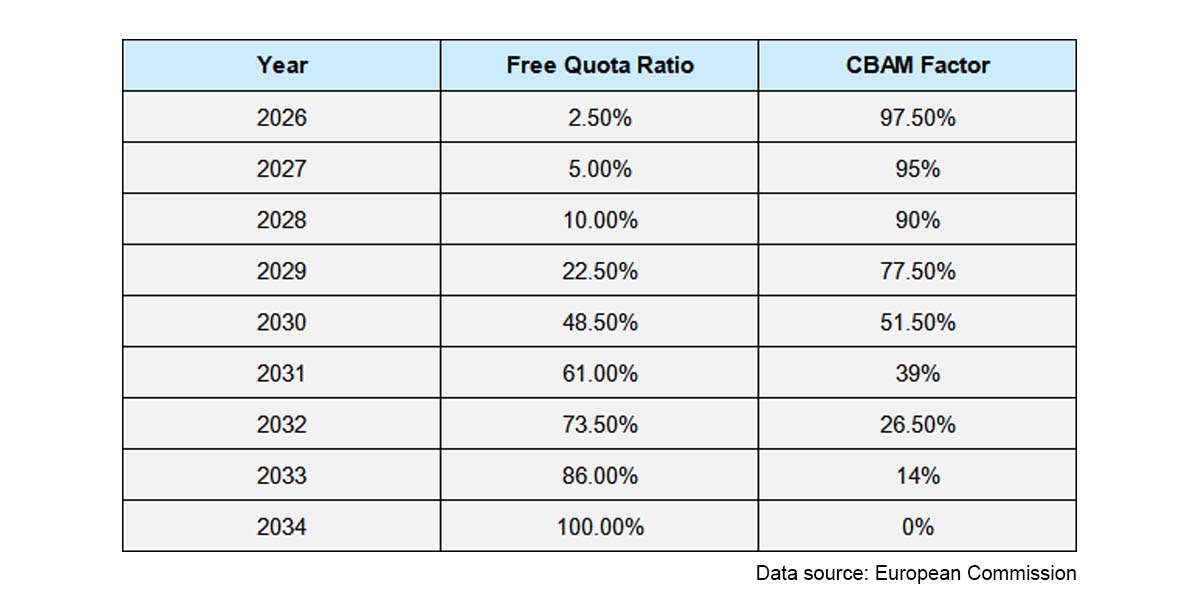

Specifically, the CBAM factor will be gradually reduced from 97.5% in 2026 to 0% by 2034, meaning that starting in 2034, importers will no longer receive free allowances and will be required to bear the full carbon cost of their implied emissions.

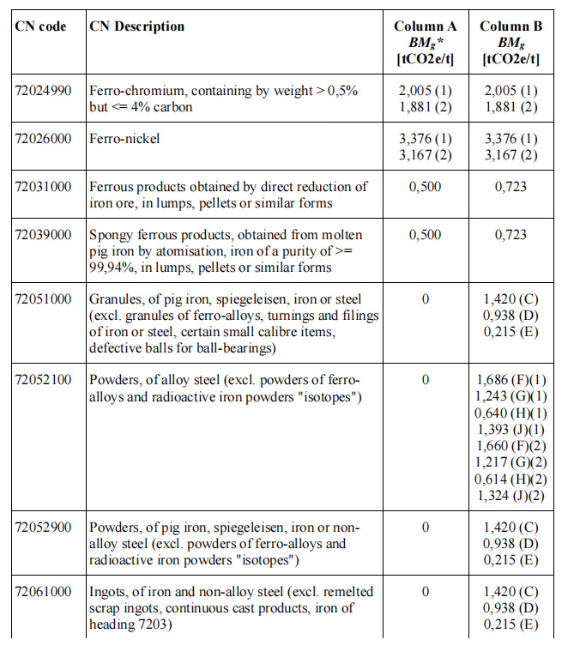

In the table below, the data in Column A and Column B are both expressed in tCO₂e/t (tonnes of carbon dioxide equivalent per tonne of product), representing carbon emission intensity under different conditions.

Analysis of the Impact on Costs for Chinese Exporters

As the world’s largest steel producer and exporter, China’s steel exports play a pivotal role in the global market and have a profound impact on the international balance of supply and demand.

The impact of CBAM on product importers lies in the requirement to declare the embodied carbon emissions of imported products and purchase corresponding CBAM certificates (i.e., pay for the implied carbon emissions of imported products), thereby directly bearing the carbon costs and compliance responsibilities linked to the EU ETS. For product manufacturers (such as Chinese exporters), the impact lies in the fact that the carbon intensity of their production processes will directly determine the cost competitiveness of their products in the EU market; low-carbon production and verifiable emissions data will become key conditions for entering the EU market.

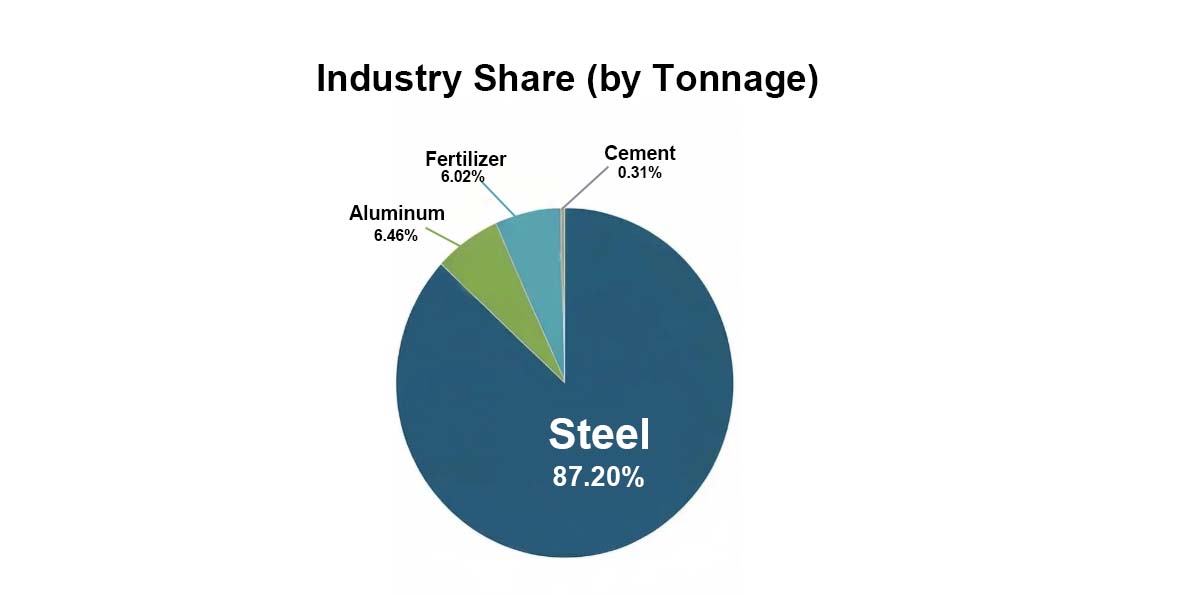

According to data from the EU’s CBAM transition period report, China is the fifth-largest exporter of products covered by the CBAM, with steel accounting for 87.2% of these exports. During the transition period, China ranked third in terms of steel export volume but first in estimated emissions. China’s steel products have the highest emissions intensity ratio, primarily because the EU has set significantly higher default emission values for Chinese products.

Implied carbon refers to indirect carbon emissions resulting from the energy consumed during a product’s production, processing, and transportation. Unlike direct emissions, it reflects a country’s responsibility for carbon emissions “exported” or “imported” through international trade.

According to calculations based on the official default carbon emission values under the EU’s Carbon Border Adjustment Mechanism (CBAM), the average carbon intensity of high-carbon products such as hot-rolled sheets and steel billets exceeds 2.8 tCO2/t of steel, which is more than double that of low-carbon products such as galvanized sheets and stainless steel. During this phase, China’s steel exports were characterized by scale expansion, primarily relying on low-cost advantages to capture international markets, with total embodied carbon emissions rising in tandem with export volumes.

Export carbon emission intensity (i.e., the embedded carbon emissions per unit of export volume) is a key indicator for measuring the level of decarbonization in steel exports. From a long-term perspective, China’s steel export carbon emission intensity has generally shown a downward trend, though there are significant variations across different phases. According to estimates, the weighted average carbon emission intensity of China’s steel exports in 2024 has fallen to approximately 1.9 tCO2/t of steel, a decrease of about 27% compared to 2005, indicating that steel export products are generally moving toward lower carbon emissions.

It is worth noting that the decline in export carbon intensity is not entirely attributable to technological progress. With the CBAM now officially in effect, Chinese steel companies are proactively adjusting their export product mix to align with the EU’s carbon accounting system—increasing the proportion of low-carbon products and reducing that of high-carbon products. This “structural reduction in emissions” will make a significant contribution to the decline in carbon intensity.

The key factor determining CBAM costs is the method used to calculate a product’s embodied carbon emissions. International buyers need to understand that whether suppliers can provide verified actual emissions data will directly determine the level of carbon costs. CBAM costs will continue to rise as the EU’s free allowances are phased out year by year. According to the implementing rules issued by the EU in December 2025, domestic steel companies in the EU are entitled to a certain proportion of free allowances under the EU Emissions Trading System (EU ETS), which effectively serves as a “discount” on the carbon cost of production within the EU. The design logic of CBAM is precisely to offset these free allowances with CBAM fees on imported products, ensuring a level playing field between domestic and imported goods. As mentioned earlier, starting in 2026, free allowances will officially enter a phase-out trajectory: a 2.5% reduction in 2026, a 5% reduction in 2027 (with the CBAM factor dropping to 95%), a reduction of nearly 50% by 2030, and a complete phase-out by 2034. This means that as free allowances decrease year by year, the CBAM costs borne by imported steel will rise annually, and the urgency of the low-carbon transition will intensify accordingly. International buyers and suppliers must ensure the transparency and traceability of carbon data when collaborating.

3. Differences in Low-Carbon Certification Standards

3.1 Terminology differentiate and analyse

Currently, the meanings of terms such as “green steel,” “low-carbon emission steel,” “low-emission steel,” and “near-zero-emission steel” remain somewhat ambiguous (as explicitly noted in a report published by the European Union’s Joint Research Centre (JRC) in April 2025). No uniform legal definition has yet been established globally; definitions vary across different literature and institutions, and there are significant differences in methodology, scope, and emission thresholds among various international initiatives and standards. For example, Muslemani et al. define “green steel” as steel products manufactured using production processes with low greenhouse gas emissions; Singh and Rout, on the other hand, define it as new steelmaking processes that reduce greenhouse gas emissions, cut costs, and improve steel quality.

This ambiguity in definitions poses numerous challenges for the market in distinguishing between products, for corporate investment decisions, and for the implementation of government policies.

Despite the variety of definitions, all of them treat carbon intensity—typically measured in carbon dioxide equivalents per ton of steel—as the core indicator for assessing the environmental performance of steel. This means that, regardless of the specific labeling terminology used, the assessment ultimately comes down to concrete carbon emission figures. Different definitions also vary in their emphasis on production processes: some definitions highlight the technological approach used in steelmaking, such as steel produced using hydrogen generated from renewable energy as a reducing agent; others link “green steel” to the principles of the circular economy, emphasizing scrap steel content as a key attribute. When making purchases, international buyers should not be misled by vague “green” labels but should instead require suppliers to provide specific carbon intensity figures and the basis for their calculations.

This ambiguity in definitions poses numerous challenges for the market in distinguishing between products, for corporate investment decisions, and for the implementation of government policies.

Despite the variety of definitions, all of them treat carbon intensity—typically measured in carbon dioxide equivalents per ton of steel—as the core indicator for assessing the environmental performance of steel. This means that, regardless of the specific labeling terminology used, the assessment ultimately comes down to concrete carbon emission figures. Different definitions also vary in their emphasis on production processes: some definitions highlight the technological approach used in steelmaking, such as steel produced using hydrogen generated from renewable energy as a reducing agent; others link “green steel” to the principles of the circular economy, emphasizing scrap steel content as a key attribute. When making purchases, international buyers should not be misled by vague “green” labels but should instead require suppliers to provide specific carbon intensity figures and the basis for their calculations.

3.2 EPD (Environmental Product Declaration)

Among the various low-carbon certification tools, the Environmental Product Declaration (EPD) is the most fundamental and internationally recognized. It provides transparent, verifiable environmental data to numerous domestic and international companies.

EPD stands for Environmental Product Declaration. It is an internationally recognized standardized report based on the ISO 14025 (Type III Environmental Labels and Declarations) standard and verified by an independent third party. It is used to quantitatively demonstrate a product’s resource consumption, emissions, and environmental impact throughout its entire life cycle (from raw material extraction to end-of-life disposal). It can be understood as a product’s “environmental ID” or “environmental passport”—a set of traceable, comparable, and audited data. Through this standardized report, environmental information for products within the same category can be compared across different regions or countries.

EPDs differ fundamentally from ordinary self-declarations or eco-labels. First, they are scientifically grounded and require quantitative analysis based on life cycle assessment. Second, they remain neutral and objective, disclosing data without assigning ratings of superiority or inferiority. More importantly, they are now regarded as the “hard currency” of green procurement in markets such as the EU and North America, serving as a crucial supporting document for international trade. Companies such as Apple, IKEA, and Volvo have already begun requiring suppliers to provide EPDs. For international buyers, requesting EPDs from suppliers effectively ensures the authenticity and reliability of carbon data and helps avoid the risk of “greenwashing.”

Domestically, the China Iron and Steel Association has established an EPD platform for the steel industry and issued Product Category Rules (PCRs) for “General Steel Products and Special Steel Products,” providing a standardized framework for domestic steel enterprises to conduct EPD verification. Third-party organizations such as the China Environmental United Certification Center and the Beijing Jianheng Certification Center have completed EPD verification for numerous steel enterprises, with the verification scope covering environmental impact data across the entire process—from raw material procurement and manufacturing to transportation. These verifications strictly adhere to international standards such as ISO 14025, ensuring the accuracy, completeness, and credibility of EPD data. For export-oriented enterprises, publishing reports through domestic EPD platforms and seeking mutual recognition with international platforms such as the EU’s can effectively reduce export compliance costs.

3.3 Overview of Mainstream International Standards for Low-Carbon Steel

The World Steel Association defines low-carbon steel as steel produced using scientific and technological methods and practical experience that results in significantly lower carbon dioxide emissions compared to traditional production methods. There is no single solution for low-carbon steelmaking; these methods can be implemented individually or in combination, depending on specific circumstances. Building on Environmental Product Declarations (EPDs), several international organizations and industry bodies have further introduced certification standards and performance grading systems for low-carbon steel. According to a report by the Resource Mobility Institute (RMI), there are currently five mainstream standards for low-carbon steel.

3.3.1. RS Standard

ResponsibleSteel is an international, non-profit, multi-stakeholder membership organization. Its certification focuses not only on greenhouse gas emissions reduction but also covers 13 environmental and social standards, including responsible sourcing of raw materials and the protection of human rights. The standard allows for certification of both sites and products. Product certification employs a sliding scale approach similar to that of the IEA, defining four greenhouse gas performance levels based on the proportion of scrap steel used, with Level 4 being the most stringent and aligning with the IEA’s net-zero emissions production standard.

3.3.2. German Low-Emission Steel Standard (LESS)

Developed by the German Steel Association, this standard has a broader system boundary than the IEA’s, covering downstream processes such as steel refining, casting, and hot rolling, and taking into account a wider range of Scope 3 emissions, such as those associated with the use of alloying agents. The standard sets different thresholds for different product categories (such as high-quality steel and structural steel). For example, for high-quality steel, the near-zero emissions threshold is 450 kg CO₂e/ton of hot-rolled steel when 0% scrap is used, and 170 kg CO₂e/ton of hot-rolled steel when 100% scrap is used. The LESS standard also introduces product labels displaying information such as performance grades, scrap content, and product carbon footprint, thereby enhancing market transparency.

3.3.3. The Global Steel Climate Council (GSCC) Steel Climate Standard

Adopts a different methodology—rather than setting absolute thresholds, it establishes decarbonization “trajectories” aligned with the IEA’s 2050 net-zero emissions scenario, setting specific emission intensity trajectories for different products, with the goal of achieving a carbon intensity of 0.12 t CO₂e/ton of hot-rolled steel by 2050. Companies must develop customized decarbonization trajectories based on their baseline-year emissions and the standard decarbonization pathway, and obtain certification following third-party verification.

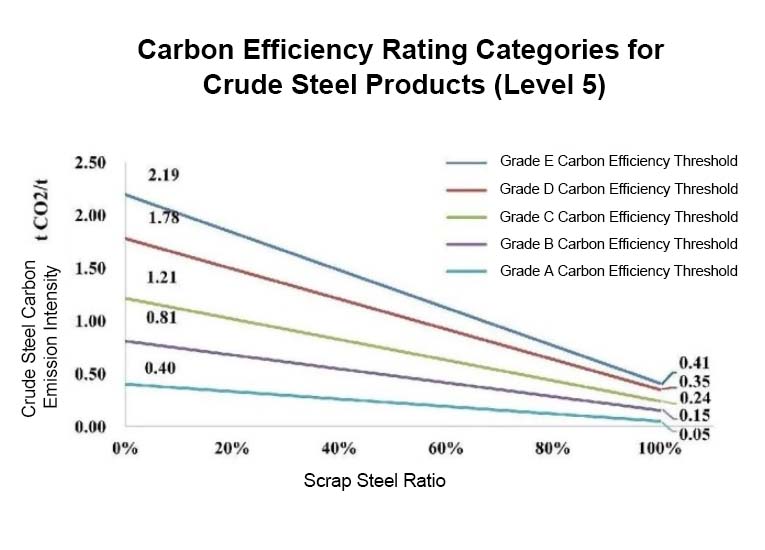

3.3.4. China’s C2F Steel Assessment Method

Jointly developed by the China Iron and Steel Association and Baowu Steel Group, this method provides a standardized framework for assessing carbon emissions from crude steel and hot-rolled products. It adopts a cradle-to-gate approach, accounting for Scope 1, Scope 2, and certain Scope 3 CO₂ emissions, and permits the use of carbon credits. Similar to the IEA, this method establishes five performance tiers based on the proportion of scrap steel used. For example, for hot-rolled products, the most stringent Class A threshold is 0.4 t CO₂e/ton of hot-rolled product when 0% scrap steel is used, and 0.05 t CO₂e/ton of hot-rolled product when 100% scrap steel is used. Products certified by a third-party assessment as meeting these thresholds may be designated as low-carbon steel.

It is worth noting that different standards exhibit significant differences in system boundaries, accounting methods, and threshold settings, which may result in the same product receiving different ratings under different standards. For example, due to broader system boundaries (covering the hot-rolling process), the thresholds set by the LESS standard are generally higher than those of the IEA standard; meanwhile, the GSCC and the Climate Bonds Initiative employ dynamic thresholds that vary over time, reflecting the trend toward convergence in emission intensities across different technological pathways by 2050.

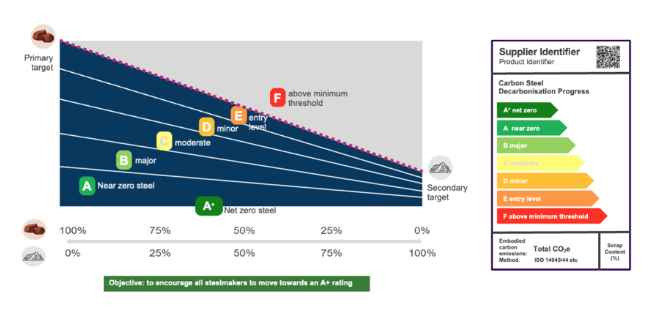

3.3.5 ArcelorMittal Low-Carbon Steel Standard

The standard proposed by ArcelorMittal is based on the following core principles:

The system uses the implicit carbon emissions per ton of hot-rolled steel (y-axis) and metal input (scrap ratio) (x-axis) as coordinates to classify steel producers into six tiers (A+ to E):

Grades A+ and A: The highest tiers, where producers may claim “net-zero” (A+) or “near-zero” (A)

Grades A through E: Progressively advancing through the decarbonization process; policymakers and customers can use this system to incentivize producers to continue decarbonizing

For international buyers, when faced with a multitude of certification standards, the following points should be kept in mind: First, prioritize EPDs that have been independently verified by a third party as the primary evidence; second, understand the methodological differences between various standards to avoid simplistic cross-comparisons; and third, work with suppliers to determine an appropriate certification pathway based on the actual circumstances of their supply chains. With the implementation of CBAM and the growing global demand for green procurement, low-carbon steel certification standards will gradually move toward harmonization and mutual recognition. However, until then, maintaining a cautious approach and demanding transparent data remains the best strategy for international buyers to mitigate the risk of “greenwashing.”

4. Case Studies of Low-Carbon Practices by Domestic and International Steel Companies

4.1 Baosteel Zhanjiang: A Million-Ton-Scale Near-Zero-Carbon Production Line

By the end of 2025, China’s first million-ton-scale near-zero-carbon steel production line was fully operational at Baosteel Group’s Zhanjiang Steel. Leveraging the hydrogen-based electric smelting process pioneered by China Baowu, the line has established a complete low-carbon metallurgical process flow comprising “hydrogen-based vertical furnace reduction—high-efficiency electric furnace smelting—low-carbon rolling production.” Using “hydrogen-based vertical furnace direct reduced iron (DRI) + scrap steel” as its primary raw materials, the line produces low-carbon slab and utilizes existing rolling facilities to manufacture low-carbon and near-zero-carbon steel products. Compared to the traditional “blast furnace + converter” long-process method of equivalent production scale, it is expected to achieve a 50%–80% reduction in carbon emissions, with the potential to cut annual carbon dioxide emissions by over 3.14 million tons. The line primarily produces high-value-added products such as high-grade automotive steel sheets and silicon steel, demonstrating that “green” and “high-end” can go hand in hand.

4.2 Shougang Jingtang: Converter Process with High Scrap Ratio

In March 2026, the “Technology for Producing High-Quality Low-Carbon Steel Bars via a Converter Process with High Scrap Ratio,” jointly developed by Shougang Jingtang and the Shougang Research Institute, was evaluated by authoritative experts from Tsinghua University and the Iron and Steel Research Institute and recognized as a globally pioneering process.

This technology pioneered a single-process, ultra-high scrap ratio smelting process in the converter without the need for additional equipment such as scrap preheating; it pioneered continuous production technology for high-quality, low-carbon steel using the long-process blast furnace–converter route, enabling stable production with ultra-high scrap ratios across multiple consecutive furnaces; and it pioneered technology for the stable control of molten steel cleanliness under ultra-high scrap ratio conditions, achieving full-coverage production of high-end products such as automotive outer panels.

With “high-scrap-ratio smelting” at its core, Shougang Jingtang has established a carbon-reduction process route with Jingtang’s distinctive characteristics, providing customers with high-quality, green steel products.

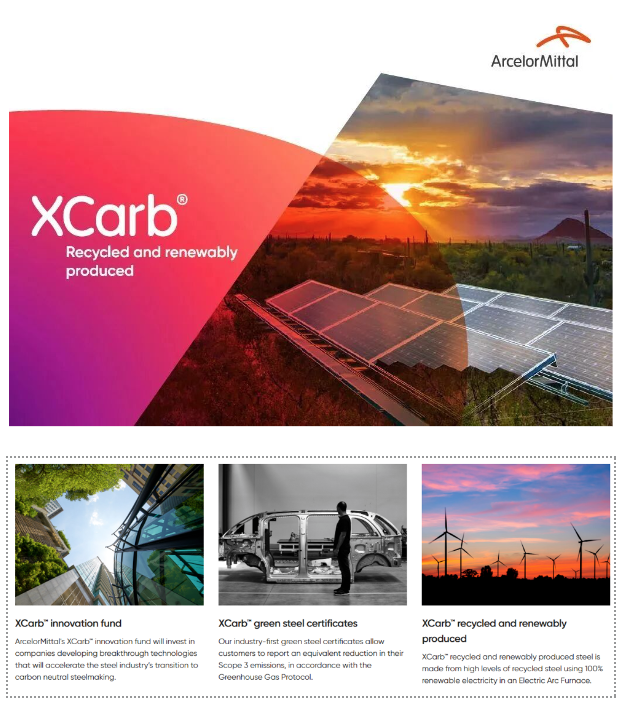

4.3 ArcelorMittal: XCarb® Innovation and Tier System

As a leading global steel company, ArcelorMittal launched the XCarb® innovation program in 2021, integrating all its carbon reduction, low-carbon, and zero-carbon products and innovation projects under a single framework. The goal is to achieve net-zero emissions (full carbon neutrality) by 2050, with a medium-term target of reducing emissions by 25-35% in Europe and North America by 2030. It also provides solutions for customers to help them achieve their own carbon reduction targets, thus demonstrating the important role of steel in the future circular economy. The general framework of this program is as follows:

XCarb®: A brand name encompassing all of ArcelorMittal's carbon reduction, low-carbon, and zero-carbon steelmaking activities, as well as broader initiatives and green innovation projects.

XCarb® Innovation Fund: Invests in companies developing breakthrough technologies that will accelerate the steel industry's transition to carbon-neutral steel.

XCarb® recycled and renewably produced: Produced in electric arc furnaces using a high proportion of scrap steel and 100% renewable electricity. Long products and most flat products are available. When the scrap ratio reaches 100%, CO₂ emissions per tonne of finished steel can be as low as approximately 300 kg.

XCarb® steel certificate: An industry-first carbon certificate mechanism designed specifically for flat steel products made from iron ore in blast furnace processes, allowing customers to claim equivalent emission reductions in Scope 3 of their emissions under the Greenhouse Gas Protocol when purchasing the certificate. By capturing and reinjecting hydrogen-rich waste gas from the steelmaking process into the blast furnace through smart carbon projects (such as Torero), the CO₂ emission reductions achieved are verified by the independent organization DNV GL and delivered to customers in the form of certificates.

Currently, the XCarb® series of products has obtained Environmental Product Declaration (EPD) certification and has been applied in multiple fields such as wind power and automobiles.

The XCarb® Innovation Program is ArcelorMittal's unified framework for integrating low-carbon products, technologies, and certifications. Through a tiered system, carbon certificate mechanism, and diverse technology pathways, it provides customers with verifiable and traceable green steel solutions.

As a unilateral climate and trade policy, CBAM directly embeds the cost of carbon emissions into international trade rules. For my country's steel and aluminum industries, this is not only an environmental requirement, but also a market access condition. Carbon management capabilities directly determine whether products can enter the EU market and at what cost.

1. Data foundation: Enterprises must establish a precise monitoring and accounting system that covers the entire process and complies with EU verification requirements as soon as possible. This means not only to solidify one's own carbon emission data foundation, but also to ensure that one can provide the implicit carbon emissions of exported products during the production process in each reporting year in order to meet CBAM's reporting requirements for "actual values".

2. Verification threshold: The CBAM data submitted by enterprises must be verified by a third-party organization certified by the competent authorities of EU member states. If the data cannot be verified, the carbon tariff can only be calculated using the default values set by the EU. Since the default values are usually significantly higher than the actual values, this will directly lead to higher carbon costs for businesses.

3.Cost pressure: The cost pressure of CBAM comes from the comparison between actual values and the baseline. When a company's actual emissions exceed the baseline of the free allowance set by the EU, the excess must be purchased by the EU importer as a CBAM certificate, resulting in direct carbon costs. More importantly, even if the goods are transshipped through a third country, they still need to be inspected and declared when they finally enter the EU, and the carbon costs are inescapable.

4. Strategic transformation: The EU’s free quota baseline for steel and aluminum products is characterized by dynamic tightening and will be lowered systematically year by year. This means that even if a company's current carbon intensity is better than the baseline, it may still face cost pressures in the future. Therefore, enterprises must regard low-carbon transformation as a long-term strategy and continuously reduce the carbon intensity of their products through the application of low-carbon technologies and process innovation in order to maintain and expand their international market share.

Carbon management capability is becoming the third core competitive advantage after price and quality. my country's steel and aluminum companies must adopt low-carbon transformation as a long-term strategy, continuously reducing the carbon intensity of their products through the application of low-carbon technologies and process innovation. Only by maintaining and expanding their international market share through low-carbon capabilities can they remain internationally competitive under increasingly stringent green trade rules.

The formal implementation of the EU Carbon Border Adjustment Mechanism (CBAM) has become a key cost variable affecting global steel exports to the EU. 2026 marks the first year of CBAM's formal implementation and a crucial window of opportunity for the global steel industry's green transformation. For international buyers, understanding CBAM policy, mastering cost accounting mechanisms, identifying low-carbon certification standards, and focusing on low-carbon best practices will help them make informed purchasing decisions in this era of challenges and opportunities.

CSMC will continue to monitor the development of CBAM green steel and actively provide useful information to its customers.

We sincerely hope that the information we provide can make more beneficial value. In addition, we sincerely invite you to leave valuable comments and advice on our website. We will follow up on your comments and advice at any time on our website.

CSMC - Empowering small and medium-scale steel purchasing.

Editor: Hana Kyra

Mail: cs@chinasteelmarket.com

|

|

|

|

|

| Timely Info | Independent | Platform | Multiple guarantees | Self-operated storage |

China Steel Market

Empowering small and medium-scale steel purchasing

| About us | Channel | Useful tools |

|---|---|---|

| About China Steel Market | Prices | Steel Weight Calculation |

| Contact Us | Answers | Why Choose Us |

| Terms & Conditions | Inventory | |

| Privacy Policy | Help |

Hot search words: