Anti-dumping is one of the core instruments of the global trade remedy system, designed to address situations where exporters sell products on the importing country’s market at prices below their normal value, thereby causing material injury to the domestic industry. From a legal perspective, anti-dumping measures have a sound basis for compliance with WTO rules; however, in practical terms, the initiation of each anti-dumping investigation or adjustment to duty rates may directly alter the price structure and competitive landscape of existing trade flows.

For international buyers, anti-dumping is no longer merely a legal risk that exporting countries or manufacturers need to address on their own. When a high anti-dumping duty is imposed on a particular product, the cost of import clearance rises significantly, the profitability of orders can change overnight, and the stability of the supply chain is also disrupted. More importantly, in recent years, major global economies have markedly intensified their anti-dumping measures against basic industrial commodities such as steel, aluminium and chemicals—with investigations being launched more frequently, covering a broader scope and resulting in higher final duty rates. Against this backdrop, purchasers who lack a systematic understanding of anti-dumping rules and developments will find it difficult to control their landed costs and will be unable to effectively assess the true risks and benefits of different supply sources.

This article aims to provide international trade practitioners with a clear and practical analytical framework. We shall discuss, in turn: the fundamental logic and legal basis of anti-dumping investigations; recent changes in the global anti-dumping landscape—specifically, how the scope, frequency and severity of such measures have escalated; the multi-dimensional impact of anti-dumping on international buyers in terms of costs, supplier selection and contract fulfilment; and, using Chinese steel products as an example, an overview of the current distribution of anti-dumping duty rates across major importing countries and regions. It is hoped that this analysis will assist readers in transforming anti-dumping from a ‘passively encountered trade barrier’ into a ‘controllable variable under proactive management’.

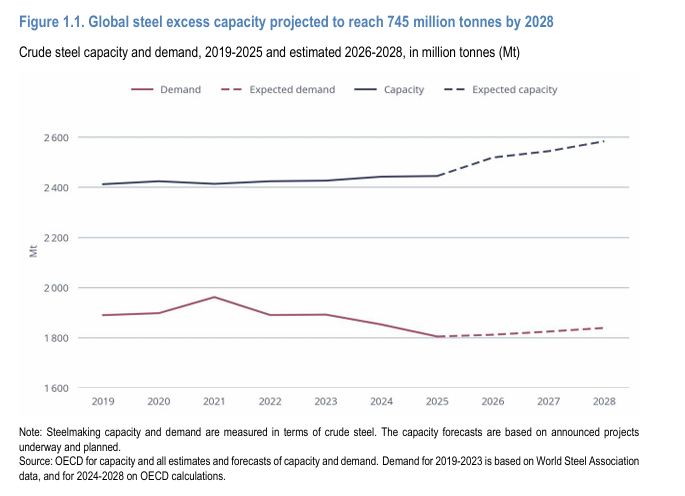

According to the OECD’s latest Steel Outlook 2026, published in June 2026, global steel overcapacity is projected to reach 745 million tonnes by 2028, exceeding the current total output of OECD member countries by 319 million tonnes. Meanwhile, between 2025 and 2028, planned new global production capacity is expected to reach approximately 139 million tonnes (an increase of 5.7 per cent), whilst demand is projected to grow at an average annual rate of only around 0.9 per cent, resulting in a widening supply-demand gap. Against this backdrop, excess capacity is being channelled into global markets through low-priced exports, placing severe competitive pressure on the equivalent industries in importing countries. Anti-dumping investigations have therefore become the most direct legal tool available to importing countries for protecting their domestic steel industries.

Matthias Coleman, Secretary-General of the OECD, stated at the OECD Ministerial Council Meeting: “Excess steel capacity creates problems for everyone. It distorts global markets, undermines economic security and resilience, and hinders innovation and sustainable development. We need to tackle the root causes, including harmful subsidies and other non-market practices. This means strengthening international cooperation to create a level playing field for steel producers around the world.”

Although China’s steel production capacity has not expanded significantly in recent years, weak domestic demand has driven a sharp rise in exports. In 2025, Chinese steel companies exported a record 131 million tonnes of steel to overseas markets, accounting for approximately 14 per cent of that year’s crude steel output and representing a 153 per cent increase on 2020. China is now once again on an expansionary path, planning to add up to 38.6 million tonnes of new capacity by 2028 (by way of comparison, this exceeds the current capacity of Italy, the European Union’s second-largest steel producer, by several million tonnes). This is expected to be the world’s largest state-led capacity expansion programme.

The legal basis for anti-dumping measures stems from the multilateral rules framework under the World Trade Organisation (WTO). The implementation of anti-dumping measures by WTO Members is primarily governed by Article VI of the General Agreement on Tariffs and Trade 1994 and the Agreement on the Implementation of Article VI of the General Agreement on Tariffs and Trade 1994 (commonly known as the Anti-Dumping Agreement). Article VI of the General Agreement on Tariffs and Trade 1994 establishes the fundamental principles of anti-dumping, whilst the Anti-Dumping Agreement sets out the procedural details for investigations and enforcement.

In accordance with the provisions of the Anti-Dumping Agreement, the investigating authority of the importing country must conduct an investigation in accordance with the requirements of the Agreement and may only impose anti-dumping duties if all three of the following conditions are met:

Firstly, the imported products are being dumped. Dumping refers to the entry of a country’s export products into the market of another country at a price below their normal value. Normal value is typically determined by reference to the comparable price of the product on the domestic market of the exporting country; if domestic sales are not representative, reference may be made to the price of exports to a third country or to constructed value (i.e. production costs plus a reasonable profit margin). Article 3 of China’s Anti-Dumping Regulations stipulates: “Dumping refers to the entry of imported products into the market of the People’s Republic of China at an export price lower than their normal value in the ordinary course of trade.” This definition is fully aligned with the WTO Anti-Dumping Agreement.

Secondly, there must be actual injury or a threat of injury to the domestic industry. The importing party must demonstrate that the domestic industry producing like products has suffered actual injury, is facing a threat of actual injury, or that the establishment of a domestic industry has been substantially impeded as a result of dumped imports. The determination of injury must be based on positive evidence; the review shall cover, amongst other things, the volume of dumped imports, their impact on the prices of like domestic products, and their impact on relevant economic indicators of the domestic industry. The investigating authority shall not attribute non-dumping factors causing injury to dumping.

Thirdly, there must be a causal link between dumping and injury. There must be a causal link between the dumped imports and the injury suffered by the domestic industry. This means that the importing party must demonstrate that it is precisely the entry of low-priced dumped products that has caused the domestic industry to suffer substantial adverse effects in terms of production volume, sales volume, profits and market share.

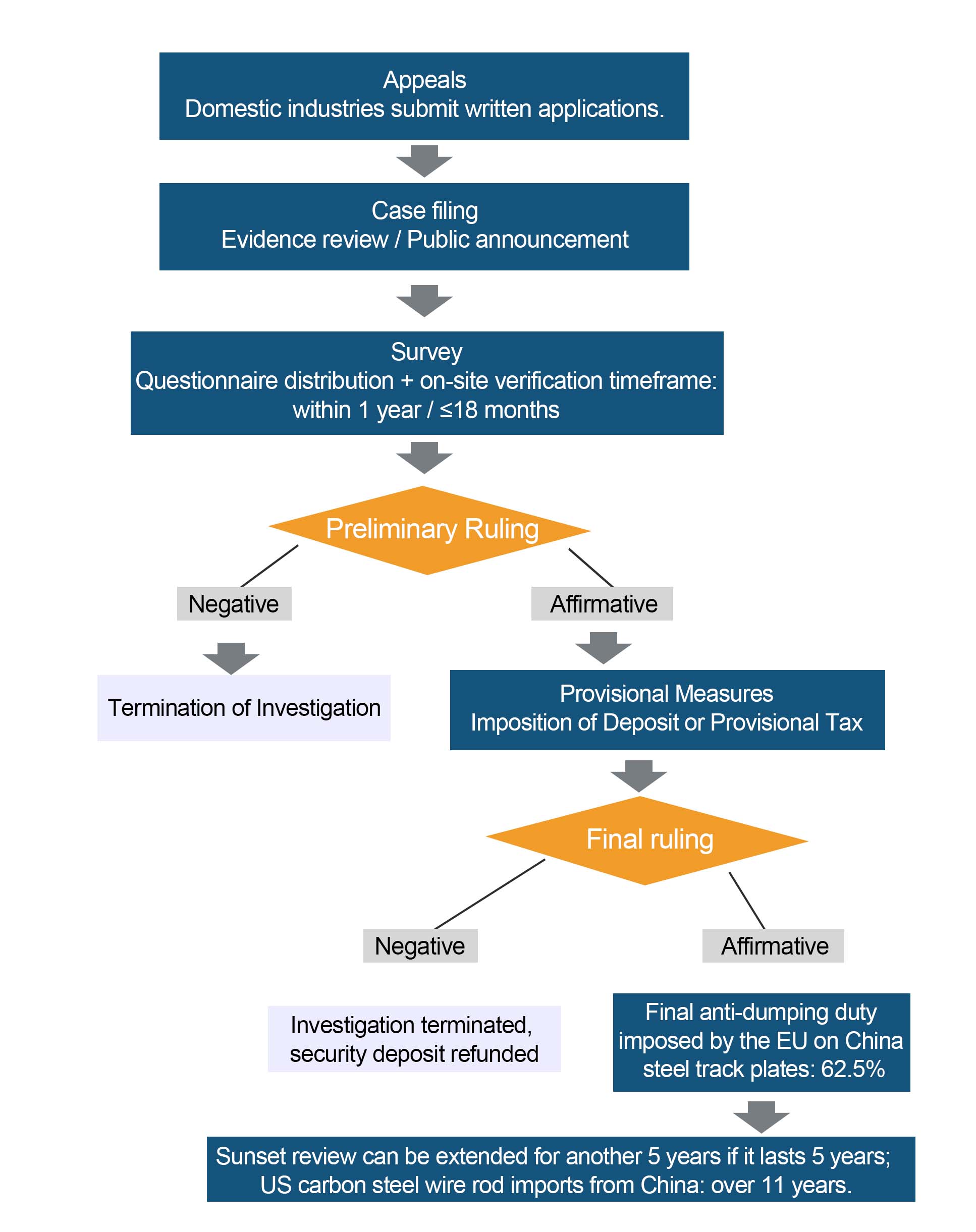

Anti-dumping investigations follow a set of procedural steps, typically comprising the stages of filing a complaint, initiation of the investigation, the investigation itself, the ruling (usually comprising a preliminary ruling and a final ruling), and subsequent reviews.

Complaint. The initiation of an anti-dumping investigation is generally triggered by a written application submitted to the relevant investigating authority by the domestic industry of the importing country or its representatives. As a general rule, the importing country’s authorities do not initiate anti-dumping investigations on their own initiative, except in exceptional circumstances. The complaint should primarily include information such as the identity of the applicant, the volume and value of production, the country of origin of the alleged product and the names of the relevant enterprises, as well as the domestic price of the alleged product.

Initiation of the investigation. After reviewing the sufficiency and authenticity of the evidence and other materials submitted with the application, the investigating authority decides whether to initiate the investigation. Once the decision to initiate the investigation has been made, the Member whose product is under investigation, as well as any interested parties known to the investigating authority, must be notified, and a public announcement must be made. The notification sent to the party under investigation shall specify the address to which the response materials are to be submitted and the relevant time limits.

Investigation. Upon receipt of an application from the complainant, the competent authority for anti-dumping investigations shall, within a specified period, investigate and verify the extent of dumping of the respondent’s products, the injury caused to the domestic industry, and the causal link between the two. This primarily involves distributing questionnaires to exporters, importers and other relevant parties, and conducting on-site inspections to verify the information. Generally, an anti-dumping investigation should be concluded within one year and, under no circumstances, shall it exceed 18 months from the commencement of the investigation.

Preliminary Rulings and Provisional Measures. Upon completion of the preliminary investigation, the investigating authority may issue a positive or negative preliminary ruling. If the preliminary ruling finds that dumping and injury have been established, provisional anti-dumping duties may be imposed or a security deposit may be required. On 22 April 2025, the European Commission issued an affirmative preliminary anti-dumping ruling on steel track plates originating in China, provisionally setting the provisional anti-dumping duty at 62.5 per cent. During the period between the preliminary and final rulings, imports of the products concerned will face additional cost pressures.

Final ruling and definitive measures. A final ruling is generally issued within 12 months of the initiation of proceedings, though this period may be extended to 18 months in exceptional circumstances. The final ruling will determine whether dumping has taken place and whether it has caused material injury to the domestic industry, and will decide whether to impose anti-dumping duties and, if so, at what rate. On 20 October 2025, the European Commission issued an affirmative final anti-dumping ruling on steel track plates originating in China, setting the final anti-dumping duty at 62.5 per cent. The investigation period for dumping in this case was from 1 July 2023 to 30 June 2024, whilst the investigation period for injury was from 1 January 2021 until the end of the dumping investigation period.

Sunset reviews and extension of measures. In principle, anti-dumping duties shall not remain in force for more than five years. Prior to the expiry of this period, if the domestic industry considers that the removal of the measures may lead to a recurrence of dumping and injury, it may apply for a sunset review (also known as an expiry review). If the review results in an affirmative determination, the measures may be extended for a further five years. This mechanism means that once anti-dumping measures are implemented, they tend to be long-term in nature. Taking the US case concerning alloy carbon steel wire rod from China as an example, the US Department of Commerce initiated anti-dumping and countervailing duty investigations into imports of alloy carbon steel wire rod from China in 2014 and issued its final determination in the same year. Subsequently, the case underwent two sunset reviews in 2019 and 2025 respectively, and the measures were maintained. On 9 December 2025, the US International Trade Commission issued an affirmative final determination on industrial injury in the second sunset review, ruling that injury would be likely to continue or recur if the current measures were repealed. From the initiation of the case to the second sunset review, the proceedings have spanned more than 11 years—for international buyers, this means that exports of the relevant products to the US have long been subject to high tariffs, leaving extremely limited scope for supply chain adjustments.

In recent years, anti-dumping measures on steel products worldwide have shown a clear trend towards escalation. This escalation is evident not only in the frequency with which investigations are initiated, but also in a number of other areas, including the expansion of the scope of countries involved, the broadening of product categories, and the rise in final duty rates. For international buyers, this means that trade policy uncertainty is continuing to increase at every stage of the supply chain.

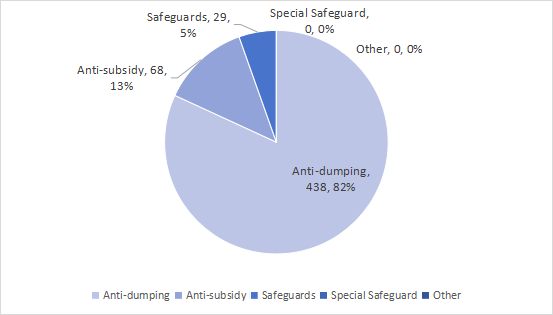

From a global perspective, the number of anti-dumping and anti-subsidy measures in force has reached an all-time high. According to data from the China Trade Remedies Information Network database, as of 2025, the number of anti-dumping measures in force in the global steel industry since 2016 stood at 438, a significant increase from the 387 recorded in 2024. Throughout 2025, a total of 58 new anti-dumping and anti-subsidy investigations were initiated worldwide. It is worth noting that the efficiency of case processing has also improved—the average time taken to reach a preliminary ruling has been reduced from 200 days in recent years to 144 days in 2025.

(The statistics presented here have been generated using data from the China Trade Remedies Information Network database and are provided for reference only.)

In terms of the countries involved, China remains the primary target. Of the 51 new anti-dumping investigations in the steel sector worldwide in 2025, 18 were directed against China, far exceeding the number targeting any other country. As of 2025, a total of 124 trade measures were in place globally against China, followed by South Korea (43) and Vietnam (33). In terms of initiating countries, a total of 18 countries launched new anti-dumping and anti-subsidy investigations into steel products in 2025, with Brazil leading the way with 15 cases, followed by Australia with 7.

In terms of specific cases, between 2025 and 2026, several major markets successively launched new investigations or issued new rulings concerning steel products; given the large number of such cases, only a selection is outlined below.

2.1.1

In June this year, Japan launched its first anti-dumping investigation into steel products from China, South Korea and Taiwan. On 1 June, the Japanese government formally announced the launch of an anti-dumping investigation into hot-rolled steel coils, cold-rolled steel coils, steel plates and steel strips imported from mainland China, South Korea and Taiwan. The investigation was jointly requested by four major steel giants: Nippon Steel, JFE Steel, Kobe Steel and Nakayama Steel. The investigation covers hot-rolled steel plates and strips used in the automotive and construction sectors, as well as cold-rolled steel plates and strips used in household appliances and automotive components. These steel products have a wide range of applications, and overproduction by Chinese firms, amongst others, has become a global issue. According to the application documents, imports of the relevant steel products from the aforementioned three regions have risen from approximately 1.23 million metric tonnes in the 2021 financial year to over 1.43 million metric tonnes recently. This represents a relatively rare trade remedy measure taken by Japan in the steel sector, signalling that a major steel-consuming market in East Asia has also joined the ranks of those adopting trade protectionist measures. Masayuki Hirose, Chairman of the Japan Iron and Steel Federation (and President of JFE Steel), stated on the same day: “We will strengthen our monitoring of unfair imports of steel whilst working with the government to explore further countermeasures.”

2.1.2

Since the beginning of this year, the EU has continued to expand the scope of products under investigation in relation to Chinese industries. On 3 June 2026, the European Commission launched an anti-dumping investigation into welded steel mesh originating in China and Turkey. Prior to this, in May 2025, the EU had formally imposed anti-dumping duties on tinplate products originating in China, with rates as high as 62.3 per cent for companies that did not cooperate with the investigation. In February 2026, the EU also issued its first final determination in the anti-dumping sunset review concerning steel wheel rims originating in China, ruling that harm would recur if the current measures were lifted. Furthermore, in April 2026, the EU initiated its third anti-dumping sunset review investigation into welded pipes of iron or non-alloy steel originating in China, Russia and Belarus.

2.1.3

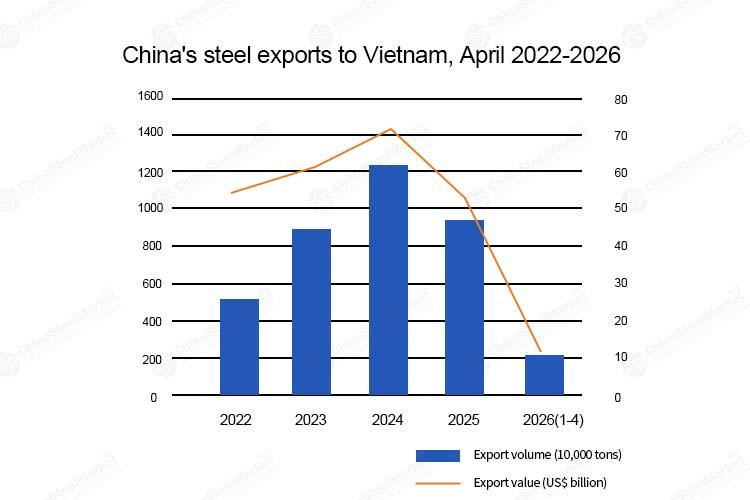

The South-East Asian market has also seen a number of sunset reviews and measure extensions. Vietnam imposed anti-dumping measures on galvanised steel sheets in August 2025 and, by the end of 2025, had completed a sunset review of anti-dumping measures on cold-rolled carbon steel coils from China, deciding to continue levying duties ranging from 4.43% to 25.22%, valid until 2030. In January 2026, Thailand issued its second final ruling on an anti-dumping sunset review, deciding to continue levying anti-dumping duties ranging from 9.24% to 20.11% on cold-rolled carbon steel coils originating in mainland China, extending the measures for a further five years. In June 2025, Malaysia issued its final ruling on the sunset review concerning cold-rolled steel coils from China, imposing anti-dumping duties ranging from 4.76% to 26.38% on Chinese products.

Whilst the frequency and scope of investigations have increased, anti-dumping duty rates have also shown a marked upward trend. The final duty rates in some cases have far exceeded conventional trade remedy levels, effectively blocking trade flows in the relevant products.

2.2.1

Extremely high tariffs imposed by the US on China are not uncommon. On 11 March 2026, the US Department of Commerce announced its final affirmative determination in the investigation into anti-dumping duties (AD) and countervailing duties (CVD) on steel fencing originating from the People’s Republic of China (China). The ruling established a dumping margin of 129.70 per cent for Chinese producers/exporters, with a nationwide uniform duty rate as high as 184.27 per cent. Furthermore, in this final anti-subsidy ruling, the subsidy rate for companies that did not participate in the proceedings reached as high as 178.97 per cent. Such triple-digit duty rates far exceed any normal commercial profit margin and effectively mean that the products in question have lost their price competitiveness in the US market.

2.2.2

Mexico’s historical duty rates on Chinese imports remain at high levels. Mexico’s anti-dumping duties on cold-rolled steel sheets from China had previously ranged from 65.99 per cent to 103.41 per cent. In February 2026, following a request from the Mexican producer Ternium México, S.A. de C.V., a new round of anti-dumping investigations was launched into cold-rolled sheet and coil originating from China, the United States and Malaysia, suggesting that these high duty rates may be maintained or further adjusted.

2.2.3

South Korea and Brazil — a combination of ad valorem and specific duties. South Korea’s provisional anti-dumping duties on hot-rolled coil from China range from 28 per cent to 33 per cent. Brazil, on the other hand, has adopted a specific duty system, imposing anti-dumping duties of between US$322.93 and US$641.73 per tonne on cold-rolled coil from China. Ad valorem duties provide greater protection against fluctuations in raw material prices, whilst also further increasing cost uncertainty for importers.

Anti-dumping duties on steel are levied on an ad valorem or specific basis and are directly factored into the additional customs clearance costs incurred by buyers on imported goods. This, in turn, drives up procurement costs for international buyers and squeezes their profit margins. When duty rates reach a certain level, supply sources that were previously price-competitive may instantly Anti-dumping duties directly increase customs clearance costs, squeeze profit margins, and when high enough, render previously competitive supply sources unviable. In November 2025, South Korea imposed 27.91%–34.10% duties on Chinese hot-rolled carbon steel plates—at the highest rate, delivered costs rose sharply. In early 2026, Brazil imposed US$284.98–709.63 per tonne on Chinese cold-rolled coils and coated steel, with duties exceeding material value for some products, forcing importers to raise prices by nearly 1,000 reais per tonne and causing flat steel imports to fall 22.6% month-on-month.

Beyond implemented measures, investigations themselves create uncertainty. In September 2025, the EU launched a probe into cold-rolled flat steel from five sources accounting for 67.7% of its imports—many buyers suspended orders. Today, duties often push landed costs up by 20–50% or more, creating a significant gap between theoretical and actual costs.

When a particular source loses its price competitiveness due to anti-dumping duties, buyers may be forced to discontinue their long-term partnerships with existing Chinese suppliers in order to When a source loses competitiveness due to duties, buyers must seek alternatives—involving due diligence, quality validation and logistics reconfiguration. Where reliance on China is high, finding alternatives matching its capacity and pricing is difficult in the short term.

The Brazilian case is illustrative: as Chinese suppliers withdrew, importers turned to Vietnam. However, when the EU simultaneously investigated five sources (India, Japan, Taiwan (China), Turkey and Vietnam) in September 2025, substitution options were severely constrained—these sources together accounted for 67.7% of EU imports. Chinese exporters' "regional restructuring and product substitution" strategy has also faced countermeasures: new growth areas such as steel billets and coated products have triggered safeguard investigations in Pakistan and Egypt. For buyers, adjusting supply sources does not guarantee security—new trade barriers may follow.

The sudden imposition or increase in anti-dumping duties often poses performance risks to existing long-term supply contracts. In most international trade contracts, price clauses are determined Sudden duty impositions or increases pose performance risks to long-term contracts. Price clauses are set based on tariffs at signing; when duties rise sharply mid-contract, sellers face cost inversion, buyers face delivery delays or price renegotiation pressures.

The EU's tinplate case is typical: in May 2025, duties ranged from 13.1%–46.8% for sampled Chinese exporters and 62.3% for non-cooperating firms—sourcing from different suppliers suddenly meant vastly different costs.Whether duties constitute force majeure depends on contract terms and applicable law. Regardless, price renegotiations and delays impose additional transaction costs. Explicit tariff risk allocation mechanisms—such as tariff variation clauses—are essential mitigation tools.

Once anti-dumping measures are implemented, they are rarely lifted in the short term. The sunset review mechanism means that the measures are subject to a review for extension every five years, and the review criterion—‘whether the lifting of the measures would be likely to lead to a recurrence of dumping and injury’—is relatively easy to satisfy. The US case concerning alloy carbon steel Once implemented, duties are rarely lifted in the short term. Sunset reviews every five years apply a relatively lenient criterion, making extensions common. The US carbon steel wire rod case from China, initiated in 2014, remains in effect after more than 11 years through two sunset reviews.

Anti-dumping measures should be viewed as long-term factors, not short-term disruptions. Buyers must identify high-risk products and markets, diversify supply sources and allocate tariff risks in contracts. Some have adopted "China plus one" strategies to diversify risk—global trade protectionism is making this capability a "must-have." Buyers must also watch derivative risks: "anti-absorption investigations" may double duties retroactively; "anti-circumvention investigations" target third-country transhipment or product modification, increasing unpredictability.

International buyers are being forced to fundamentally restructure procurement strategies, accelerating diversification to enhance resilience. While exporters bear the direct brunt, the impact extends across costs, supply chains, contract performance and compliance—understanding these is the prerequisite for effective response strategies.

Based on their respective industrial policies and legal frameworks, various countries impose anti-dumping duties on different types of steel products. Not only do these duty rates vary by product, but the methods and levels of imposition also exhibit distinct characteristics by country and region.

The following is a summary of major rulings in recent years, organised by country, for reference in procurement decisions. Please refer to the latest official announcements from each country for specific details.

On 2 April 2026, the Vietnamese Ministry of Industry and Trade issued Announcement No. 612/QD-BCT, reaching an affirmative preliminary ruling on anti-circumvention proceedings concerning hot-rolled coil originating in China. It preliminarily determined that the products in question had undergone minor alterations to circumvent anti-dumping duties, and imposed a provisional anti-dumping duty of 27.83 per cent on hot-rolled coil with a width exceeding 1,880 millimetres but not exceeding 2,300 millimetres. The measures shall take effect 15 days after the publication of the notice.

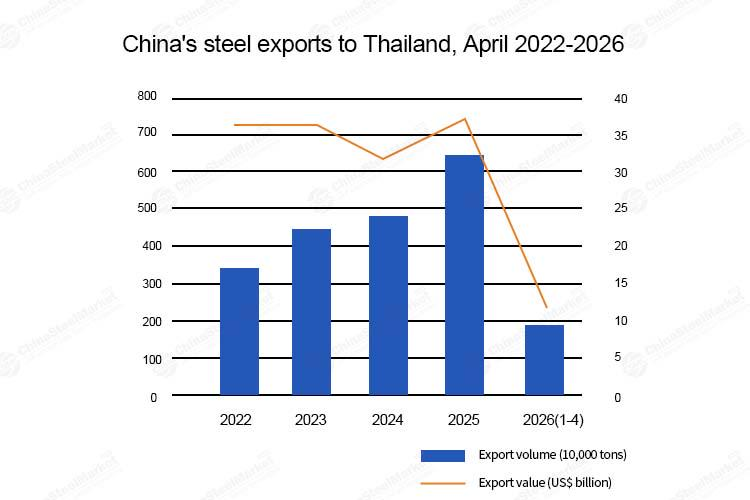

Thailand is one of the most important export markets for Chinese steel in South-East Asia. In 2025, the value of China’s steel exports to Thailand reached US$3.82 billion, representing a year-on-year increase of 13.5 per cent, with Thailand ranking among the top five destinations for Chinese steel exports. However, Thailand has frequently initiated anti-dumping and anti-circumvention investigations into Chinese steel products in recent years, and the export environment for Chinese steel enterprises in the Thai market has become increasingly challenging. Between January and April 2026, Chinese exports of coated steel sheets to Thailand had already fallen by 16.3 per cent year-on-year.

On 26 May 2026, Thailand issued its second affirmative final ruling in the anti-dumping sunset review concerning high-carbon wire rod originating in China, deciding to continue levying anti-dumping duties at rates ranging from 12.26% to 36.79% on a CIF basis for a period of five years. Specifically, the rate for Benxi Beitai High-Speed Wire Rod Co., Ltd. is 12.26 per cent; for companies under the Jiangsu Shagang Group, 15.04 per cent; for Jiangsu Yonggang Group, 20.56 per cent; and for other companies, 36.79 per cent.

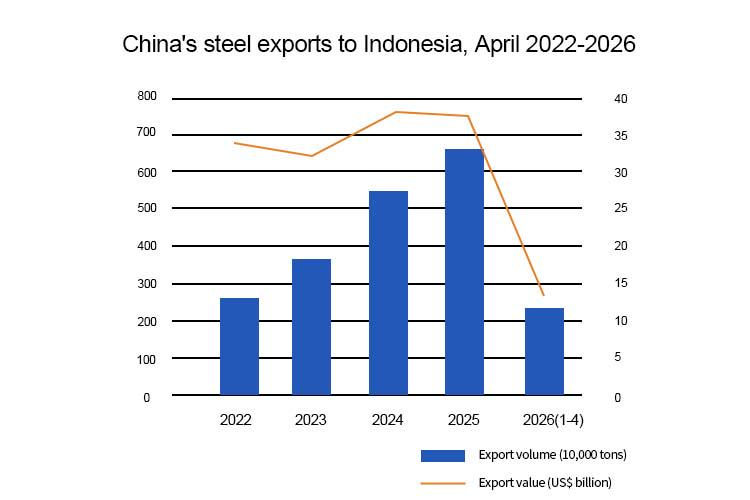

Indonesia is a major economy in South-East Asia. In recent years, its economy has maintained steady growth, driving demand for steel across various domestic industries. Sectors such as infrastructure, property, automotive, electronics and household appliances have developed rapidly, generating significant demand for steel. Furthermore, Indonesia is a key partner in the ‘Belt and Road’ initiative and a member of ASEAN; it is also deeply involved in regional free trade agreements such as the RCEP and the CPTPP. Indonesia is emerging as one of the best options for Chinese steel enterprises looking to expand overseas. In recent years, the volume of Chinese steel exports to Indonesia has grown steadily;

however, Indonesia has also launched anti-dumping investigations into Chinese steel products in recent years. On 22 May 2026, the Indonesian Ministry of Finance issued Announcement No. 32 of 2026, deciding to impose a provisional anti-dumping duty of 17.50 per cent on hot-rolled coils of iron or non-alloy steel produced by Wuhan Iron and Steel Co., Ltd.

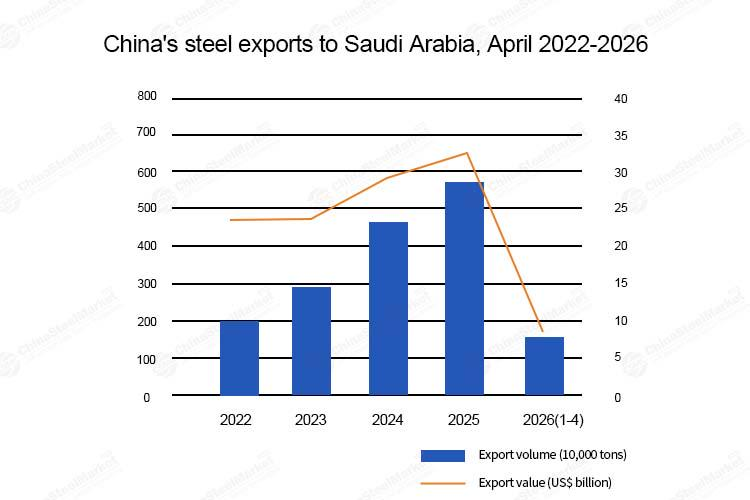

Against a backdrop of escalating global protectionism, with many countries imposing additional tariffs on Chinese steel products and launching a flurry of anti-dumping and anti-subsidy investigations, Saudi Arabia has rapidly emerged as a key destination for Chinese steel exports, thanks to its relatively open trade environment and the sustained surge in infrastructure demand driven by ‘Vision 2030’.

In 2025, the volume of steel exported from China to Saudi Arabia increased by 23.7 per cent year-on-year to 5.7496 million metric tonnes, whilst the value of exports rose by 12.2 per cent year-on-year to US$3.27 billion

The General Authority for Foreign Trade (GAFT) of Saudi Arabia announced the imposition of definitive anti-dumping duties on imports of round-section steel or stainless steel pipes originating in China. These duties will take effect on 30 June 2025 and remain in force for five years. As part of this decision, the General Authority for Tax and Customs has imposed duties ranging from 6.5 per cent to 27.3 per cent, depending on the manufacturer.

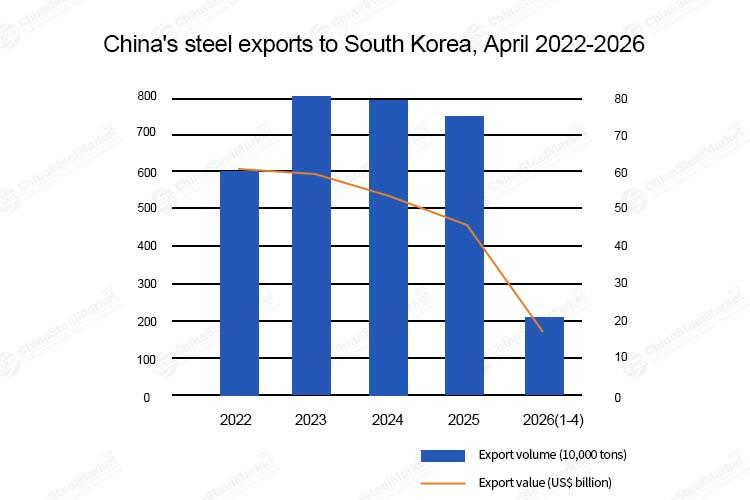

South Korea has long been one of China’s key export markets for steel. In recent years, South Korea has frequently initiated ‘anti-dumping and anti-subsidy’ investigations into Chinese steel products and imposed high tariffs, leading to a decline in the export share of Chinese steel enterprises in the South Korean market; however, this share remains at a relatively high level.

On 12 June 2026, South Korea’s Ministry of Strategy and Finance issued Announcement No. 2026-80, deciding to impose a four-month provisional anti-dumping duty on cold-rolled steel coated with zinc or zinc alloys (Cold-rolled products of carbon steel or alloy steel surface-treated with zinc or zinc-alloys) originating in China, effective from 12 June 2026 to 11 October 2026.

Specifically, the duty rate for Inner Mongolia Baotou Steel Union Co., Ltd. and its affiliated enterprises is 22.34 per cent, Shougang Jingtang United Iron & Steel Co., Ltd. and its affiliated enterprises are subject to a rate of 26.28 per cent; Winstone Development Ltd. (Hong Kong, China) is subject to a rate of 33.67 per cent; and other producers/exporters are subject to a rate of 25.75 per cent.

Faced with the ongoing escalation of anti-dumping investigations into Chinese steel by countries around the world, international buyers are confronting multiple challenges, including rising procurement costs, supply chain instability and heightened compliance risks. International buyers need to shift from a passive stance to proactive management, transforming anti-dumping from a ‘trade barrier’ into an external driver for supply chain optimisation and the development of compliance capabilities.

How can you maintain competitiveness, mitigate risks and optimise procurement decisions within the new trade landscape?

Please feel free to contact our trade specialists to obtain bespoke strategies and real-time alerts.

Whatsapp&Wechat:+86-18864881658

Email: cs@chinasteelmarket.com

Disclaimer: All information cited in this feature is sourced from public and legitimate channels, including but not limited to official announcements from various countries, the China Trade Remedies Information Network, China Customs statistics and public reports from the Organisation for Economic Co-operation and Development (OECD), and is intended to serve as a general reference for those working in international trade. This platform does not guarantee the complete accuracy, completeness or timeliness of all information. The relevant data and political developments are based on publicly available information as of June 2026 and may be subject to change due to policy adjustments or other factors; please refer to the latest official announcements from the respective countries.

The content of this special feature is for reference only and does not constitute investment advice, trade decision-making advice or legal advice of any kind. The information provided in the report, including but not limited to data, views and text, does not constitute legal evidence. Before making procurement decisions, signing contracts or taking other commercial decisions, users should exercise independent judgement based on their own circumstances and may consult trade compliance experts. This platform accepts no liability for any actions taken by users based on the content of this special feature, nor for any direct or indirect losses arising therefrom.

We sincerely hope that the information we provide can make more beneficial value. In addition, we sincerely invite you to leave valuable comments and advice on our website. We will follow your comments and advice at any time on our website.

CSMC-Empowering small and medium-scale steel purchasing.

Editor: Hana Kyra

Mail: cs@chinasteelmarket.com

|

|

|

|

|

| Timely Info | Independent | Platform | Multiple guarantees | Self-operated storage |

China Steel Market

Empowering small and medium-scale steel purchasing

| About us | Channel | Useful tools |

|---|---|---|

| About China Steel Market | Prices | Steel Weight Calculation |

| Contact Us | Answers | Why Choose Us |

| Terms & Conditions | Inventory | |

| Privacy Policy | Help |

Hot search words: